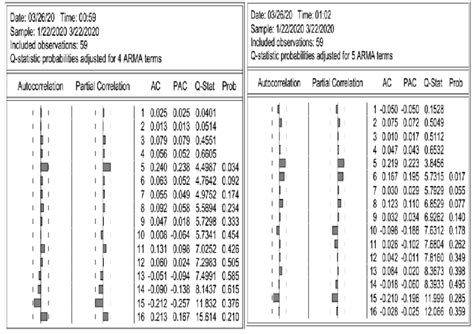

r box.test|ljung box test white noise : online sales Compute the Box--Pierce or Ljung--Box test statistic for examining the null hypothesis of independence in a given time series. These are sometimes known as ‘portmanteau’ tests. 22 de dez. de 2022 · 1. Entrega atrasada. Primeiramente, faça seu login, vá em “Meus pedidos”, escolha o pedido desejado e clique em "Ver". Lá você encontra o .

{plog:ftitle_list}

39 anos. Ola minha pri vez anunciado mim chamo bia sou uma acompanhante bem educada atenciosa cheirosa, adoro foder gostoso vem me conhecer . Serrinha - BA. R$ 150 /h. Sem vídeo de comparação.

Compute the Box--Pierce or Ljung--Box test statistic for examining the null hypothesis of independence in a given time series. These are sometimes known as ‘portmanteau’ tests.Description. box.test performs Box F test. Usage. box.test(formula, data, alpha = 0.05, na.rm = TRUE, verbose = TRUE) Value. A list with class "owt" containing the following components: .Box-Pierce and Ljung-Box Tests Description. Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in a given time series. These are .In this article, we will learn how to perform a Ljung-Box test in R. The Ljun-Box test is a hypothesis test that checks if a time series contains an autocorrelation. The null Hypothesis H0 is that the residuals are independently distributed.

Description. If pierce is TRUE, then the Box-Pierce test for examining the null of independence in the time series x is computed. Else the Box-Ljung statistic is computed. Uses lag .The Ljung–Box test (named for Greta M. Ljung and George E. P. Box) is a type of statistical test of whether any of a group of autocorrelations of a time series are different from zero. Instead of .

Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in a given time series. Usage Box.test(x, lag = 1, type = c("Box-Pierce", "Ljung .Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in a given time series. These are sometimes known as ‘portmanteau’ tests.

Description. Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in a given time series. These are sometimes known as ‘portmanteau’ tests. .The Ljung-Box test is used to check if exists autocorrelation in a time series. The statistic is q = n(n+2)\cdot\sum_{j=1}^h \hat{\rho}(j)^2/(n-j) with n the number of observations and \hat{\rho}(j) the autocorrelation coefficient in the sample when the lag is j.Box.test {stats} R Documentation \IBox-\IPierce and \ILjung-\IBox Tests Description. Compute the \IBox–\IPierce or \ILjung–\IBox test statistic for examining the null hypothesis of independence in a given time series. These are sometimes known as ‘portmanteau’ tests. Usage

This article describes how to do a t-test in R (or in Rstudio).You will learn how to: Perform a t-test in R using the following functions : . t_test() [rstatix package]: a wrapper around the R base function t.test().The result is a data frame, which .How to run a Box-Tidwell test in R to test for a linear relationship between the independent variables and log odds? 0. Logistic regression in R, Stan. 1. write a r function to run regression. 0. Apply logistic regression in a function in R. Hot Network Questions Undead UniformsboxM performs the Box's (1949) M-test for homogeneity of covariance matrices obtained from multivariate normal data according to one or more classification factors. The test compares the product of the log determinants of the separate covariance matrices to the log determinant of the pooled covariance matrix, analogous to a likelihood ratio test.

To perform the test in R the function Box.test() can be used with the following syntax: Box.test(ts, lag = number_of_lags, type = "Ljung-Box") Instrucciones 100 XP. Test \(H_0\): "There is no autocorrelation left in final_model_resid" using the Ljung-Box test with the rule of thumb from above;The Ljung-Box (1978) modified portmanteau test. In the multivariate time series, this test statistic is asymptotically equal to Hosking . Rdocumentation. powered by. Learn R Programming. portes (version 6.0) Description . Usage Value. Arguments, , .

I want to conduct the Ljung-Box test on residuals of the ARIMA model with. Box.test(e, type = "Ljung-Box", fitdf = degrees_of_freedom) where N = 3064, with 8 variables and additional 1 adjustmend from ar(1) in ARIMA model.

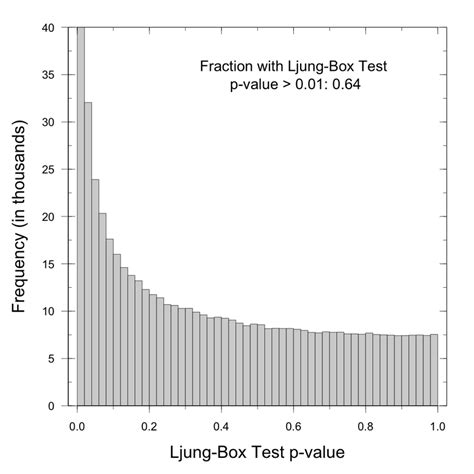

Here is an example of The Ljung-Box test: . Here is an example of The Ljung-Box test: . Learn / Courses / Quantitative Risk Management in R. Course Outline. 1. Exploring Market Risk-Factor Data Free. 0%. In this chapter, you will learn how to form return series, aggregate them over longer periods and plot them in different ways. You will look . This is an indication that the residuals of the box-cox transformed model are much more normally distributed, which satisfies one of the assumptions of linear regression. Additional Resources. How to Transform Data in R (Log, Square Root, Cube Root) How to Create & Interpret a Q-Q Plot in R How to Perform a Shapiro-Wilk Test for Normality in R Escanciano and Lobato constructed a portmanteau test with automatic, data-driven lag selection based on the Pierce-Box test and its refinements (which include the Ljung-Box test). The gist of their approach is to combine the AIC and BIC criteria --- common in the identification and estimation of ARMA models --- to select the optimal number of .

what is ljung box test

The calculations required for Box’s test are given in Figure 2. Figure 2 – Box’s test for Example 1. m = number of matrices = 3 (Young, Middle, Old), k = the size of each covariance matrix = 5 (each matrix is 5 × 5), n 1 = n 2 = n 3 = number of subjects in each sample = 7 and so n = n 1 .

Plots the p-values Ljung-Box test. Rdocumentation. powered by. Learn R Programming. LSTS (version 2.1) Description. Usage Arguments Value. Details. . References. See Also. Examples Run this code # NOT RUN {Box.Ljung.Test(malleco, lag = 5) # } Run the .Box.test.2 computes at different lags, a Portemanteau statistic for testing that a time series is a white noise. RDocumentation. Learn R. Search all packages and functions . (123) y1 <- arima.sim(n = 100, list (ar = -.7), sd = sqrt (4)) a1 <- Box.test.2(y1, nlag = c (3, 6, 9, 12), type = "Ljung-Box", decim = 4)Weighted portmanteau tests for testing the null hypothesis of adequate ARMA fit and/or for detecting nonlinear processes. Written in the style of Box.test() and is capable of performing the traditional Box Pierce (1970), Ljung Box (1978) or Monti (1994) tests.

Box.test {ts} R Documentation: Box–Pierce and Ljung–Box Tests Description. Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in the time series x is computed. Usage Box.test (x, lag = 1, type=c("Box-Pierce", "Ljung-Box"))

This function modifies the Box.test function in the stats package, and it computes the Ljung-Box or Box-Pierce tests checking whether or not the residuals appear to be white noise. Rdocumentation. powered by. Learn R Programming. TSA . (1, 0, 0)) LB.test(m1.color) # } Run the code above in your browser using .However, Ljung-Box test doesn't look good for , for instance, 20 lags: Box.test(resid(fit1),type="Ljung",lag=20,fitdf=1) I get the following results: X-squared = 26.8511, df = 19, p-value = 0.1082 To my understanding, this is the confirmation that the residuals are not independent ( p-value is too big to stay with the Independence Hypothesis).ljung_box {feasts} R Documentation: Portmanteau tests Description. Compute the Box–Pierce or Ljung–Box test statistic for examining the null hypothesis of independence in a given time series. These are sometimes known as ‘portmanteau’ tests. Usage ljung_box(x, lag = 1, dof = 0, .) box_pierce(x, lag = 1, dof = 0, .) portmanteau_tests .Box's approximation seems to be good if each n_i exceeds 20 and if k and p do not exceed 5 (Bibby and Kent (1979) pg. 140). Value A vector with the the test statistic, the p-value, the degrees of freedom and the critical value of the test.

Box's M-test Description. boxM performs the Box's (1949) M-test for homogeneity of covariance matrices obtained from multivariate normal data according to one or more classification factors. The test compares the product of the log determinants of the separate covariance matrices to the log determinant of the pooled covariance matrix, analogous to a likelihood ratio test.box.test Box-Pierce 和 Ljung-Box 测试 Description. 计算 Box-Pierce 或 Ljung-Box 检验统计量,以检查给定时间序列中的 null 独立性假设。这些有时被称为“混合”测试。

The R sarima command will give a graph that shows p-values of the Ljung-Box-Pierce tests for each lag (in steps of 1) up to a certain lag, usually up to lag 20 for nonseasonal models. Interpretation of the Box-Pierce Results. Notice that the p-values for the modified Box-Pierce all are well above .05, indicating “non-significance.”

When reading ?Box.test, I learned about a rarely mentioned parameter fitdf, which specified the "number of degrees of freedom to be subtracted if x is a series of residuals".It seems that when applying this function on residuals, we should pass this parameter to Box.test.. Details. These tests are sometimes applied to the residuals from an ARMA(p, q) fit, in which case the .The univariate or multivariate Box-Pierce (1970) portmanteau test. Rdocumentation. powered by. Learn R Programming. portes (version 6.0) Description. Usage Value. Arguments, , , . ## Correct ## ## ## Monthly log stock returns of Intel corporation data: Test for ARCH Effects monthintel <- as.ts(monthintel) BoxPierce .

ljung box test white noise

Tukey test is a single-step multiple comparison procedure and statistical test. It is a post-hoc analysis, what means that it is used in conjunction with an ANOVA. It allows to find means of a factor that are significantly different from each other, comparing all possible pairs of means with a t-test like method.

We would like to show you a description here but the site won’t allow us.

Resultado da 1 de fev. de 2024 · A Claro NET Combo Multi é o serviço que junta os planos da NET e Claro, tornando possível que você tenha acesso a uma variedade maior de serviços. Nele, pode conter planos de TV por assinatura, telefonia fixa, internet banda larga e telefonia móvel (planos controle ou pós-pago). .

r box.test|ljung box test white noise